November 8, 2023 – The third quarter marks the beginning of a new era in the history of D&L Industries, with the commercial operations of its new plant in Batangas which issued its first invoice last July. With upgraded capabilities specced to the highest standards and a footprint that will more than double the company’s existing manufacturing capacity, the new plant positions D&L as a truly world-class Filipino manufacturing company.

Short-term pain, long-term gain; 9M results mask new plant’s potential

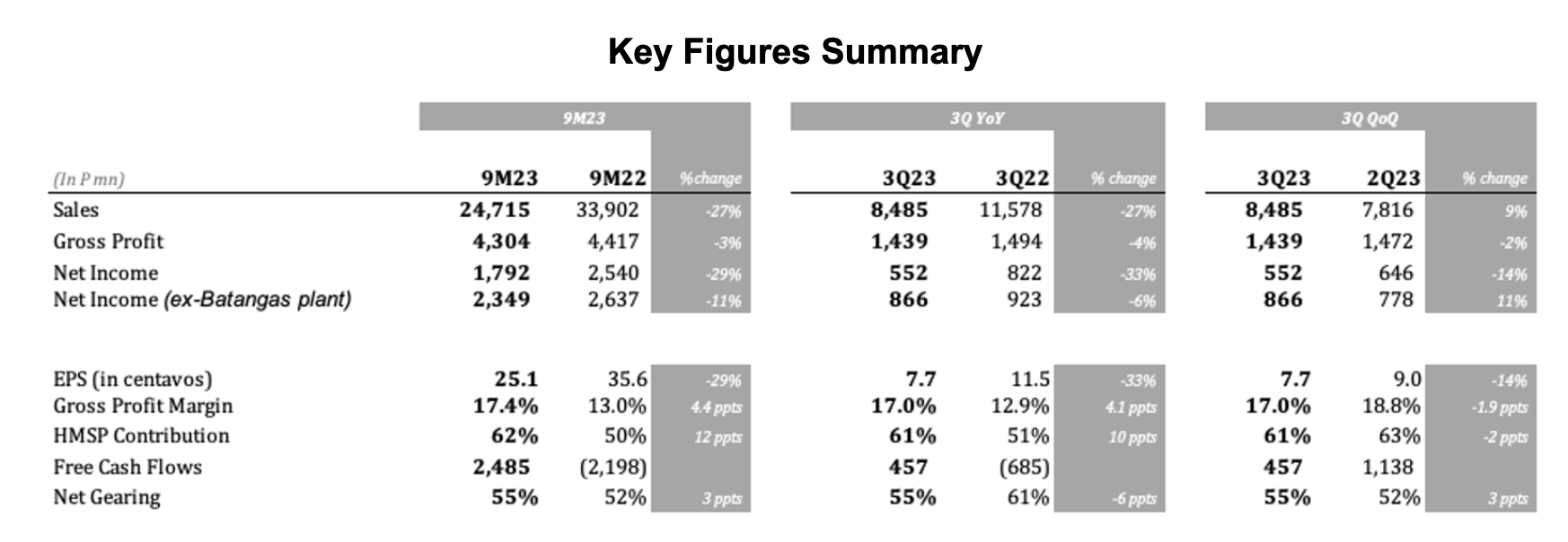

In the first nine months of the year (9M23), D&L Industries’ recurring income reached P1.8 billion, or earnings per share of P0.25, lower by 29% YoY. The drop in earnings was mainly due to the challenging business environment with the lingering effects of high inflation coupled with the incremental expenses related to the commercial operations of its Batangas plant. Excluding the Batangas plant, earnings would have fallen by just 11% YoY to P2.3 billion for the quarter.

“While incremental expenses are more apparent at the start of operations of a new plant, we have confidence that this will be a huge benefit to the company, as what we have seen multiple times over the past 60 years,” D&L President and CEO Alvin Lao remarked.

“We see the near-term weakness in earnings masking the potential of the new plant. At the same time, we see an opportunity with the concurrent weakness in share price for long-term and value investors like us. The family, through Jadel holdings, continues to buy shares of the company as what you’d see in our recent disclosures,” Lao added.

“We believe that there has never been a more exciting time for D&L. Our Batangas plant will allow us to explore opportunities that were previously beyond our existing capabilities. With the new plant, we will open new markets, expand our range of higher value added products, and deepen innovations that will further push our boundaries. We are profoundly inspired by its potential and we are steadfast in our commitment to see it to fruition,” Lao reiterated.

Batangas plant is D&L’s next leg of growth

D&L’s Batangas plant sits on a 26-ha property in First Industrial Township – Special Economic Zone in Batangas. This facility will mainly cater to D&L’s growing export businesses in the food and oleochemicals segments. It will add the capability to manufacture downstream packaging, thus allowing the company to capture a bigger part of the production chain. For instance, while the company primarily sells raw materials to customers in bulk, the new plants will allow it to “pack at source”. This means that D&L will have the ability to process the raw materials and package them closer to finished consumer-facing products. This will enable D&L to move a step closer to its customers by providing customized solutions and simplifying their supply chain, which is of high importance given ongoing logistical challenges.

The new plant will also be instrumental in D&L’s goal of putting the Philippines on the map as a quality manufacturing hub for sustainable, natural and organic products. The company is gearing up towards launching a full range of shelf-ready products for its export customers, made from coconut oil, for the personal and baby care, cosmetics and beauty care, household cleaning, health and nutrition, and food and vegetable oils categories that are sustainable, natural, and organic. This initiative offers a plug-and-play solution for global brand owners who are looking to beef up their sustainable product offerings. D&L targets export sales to account for at least 50% of total revenues in the long-term.

D&L’s Batangas facility

Sequential recovery continued

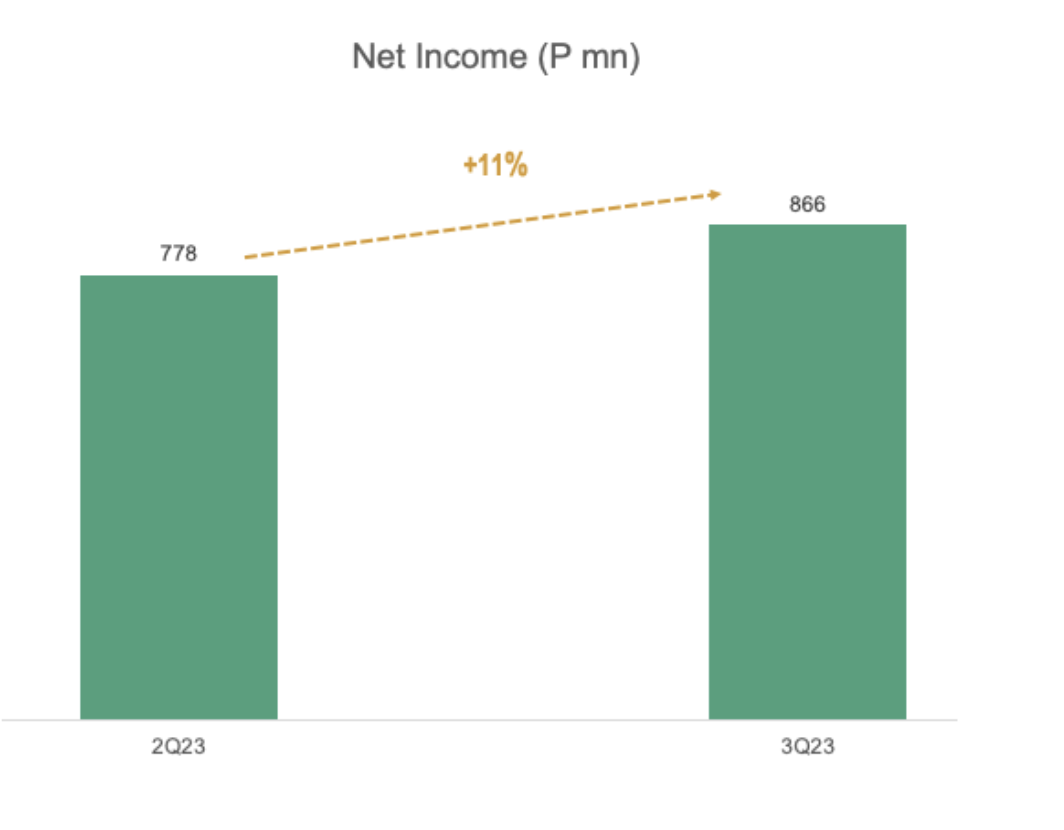

While the environment remains tough given the lingering effects of high inflation and generally cautious consumer sentiment, sequential recovery continued with 3Q23 earnings ex-Batangas plant up 11% QoQ. This was mainly driven by a rebound in High Margin Specialty Products (HMSP) and commodity volumes which were up 11% QoQ and 23% QoQ, respectively.

On a YoY basis, food ingredients, specialty plastics, and aerosols have all posted higher earnings for the quarter. For food ingredients, the improvement was mainly coming from better margins given the normalization of commodity prices after a period of volatility and a pick up in HMSP volume as the food industry continues to recover. For specialty plastics, the normalization of semiconductor supply globally has prompted a bounce back in the demand for engineered polymers used for automotive applications. For consumer products ODM, the continued opening up of the economy and resumption of face-to-face activities have resulted in a surge in demand for various personal care products.

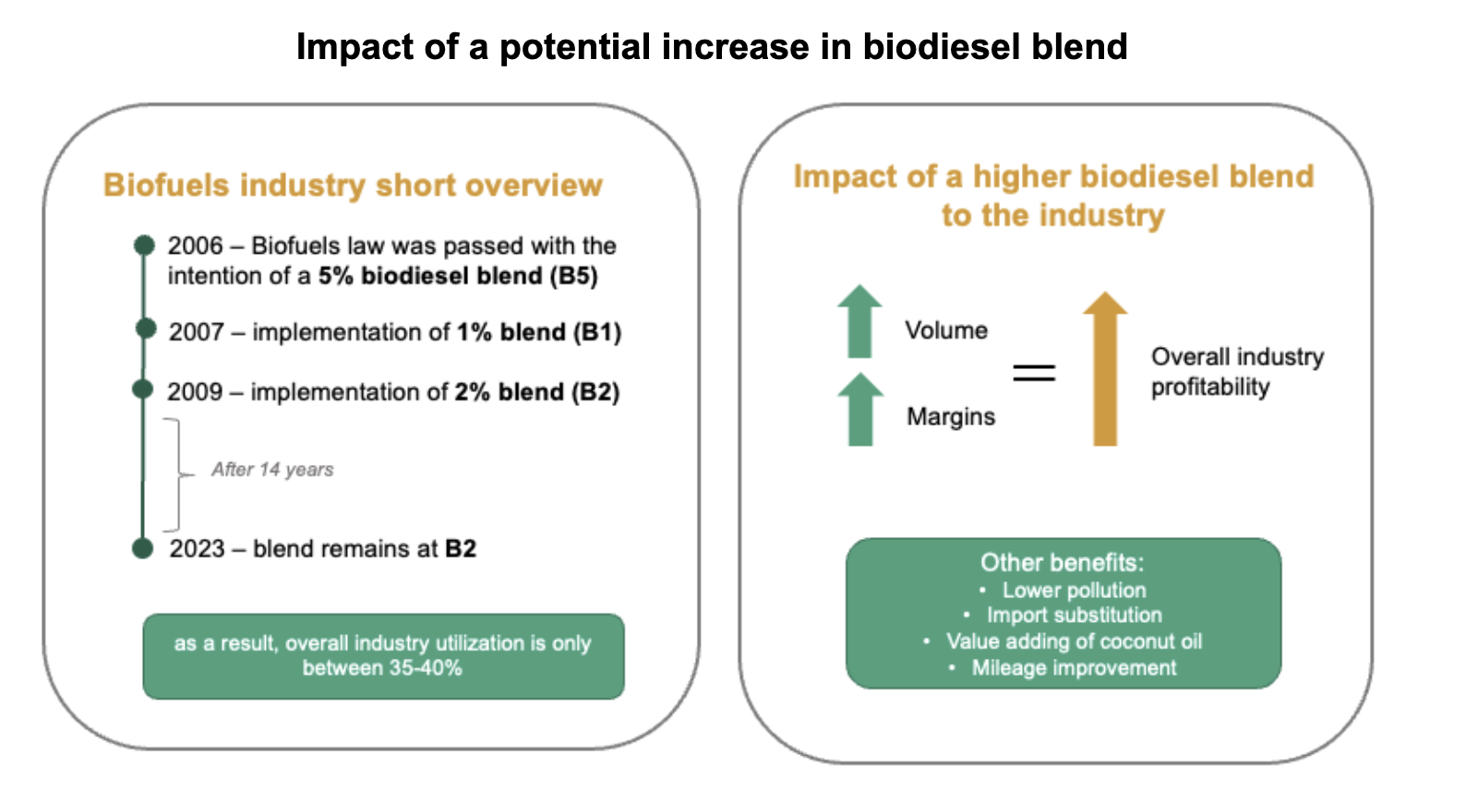

Potential increase in biodiesel blend, a catalyst on the horizon

With the average price of Brent crude oil up 29% from pre-pandemic levels, the Philippines, as a big importer of oil, is currently considering a wide array of measures on how to mitigate the effects of higher fuel prices while reducing the country’s dependence on imported fuel. One of the measures being considered by the government is the increase in mandated biodiesel blend from two percent (2%) to three percent (3%).

In 2006, the Biofuels law was passed. Among its provisions, is the requirement to blend biodiesel from 100% local coconut oil feedstock to every liter of diesel sold in the country. A one percent (1%) biodiesel blend was initially implemented in 2007. It was increased to a two percent (2%) blend in 2009. As per the country’s biofuels roadmap, the target was to eventually increase the blend to reach five percent (5%).

With the expectations that the blend requirement will more than double from 2009 level, the industry has built up capacity to meet the anticipated demand. However, 14 years have passed and the biodiesel blend has remained stagnant at 2%. As a result, the biodiesel industry has been operating in an oversupply environment for many years now. Overall industry utilization is estimated between 35%-40%. A potential increase in blend to three percent (3%), all else being equal, in theory should lead to a 50% increase in biodiesel volumes which may also result in better margins and profitability for the industry. D&L, through its subsidiary Chemrez, is a big player in the biodiesel industry.

Meanwhile, other benefits of a higher biodiesel blend include lower pollution, import substitution, value adding of coconut oil, and mileage improvement.

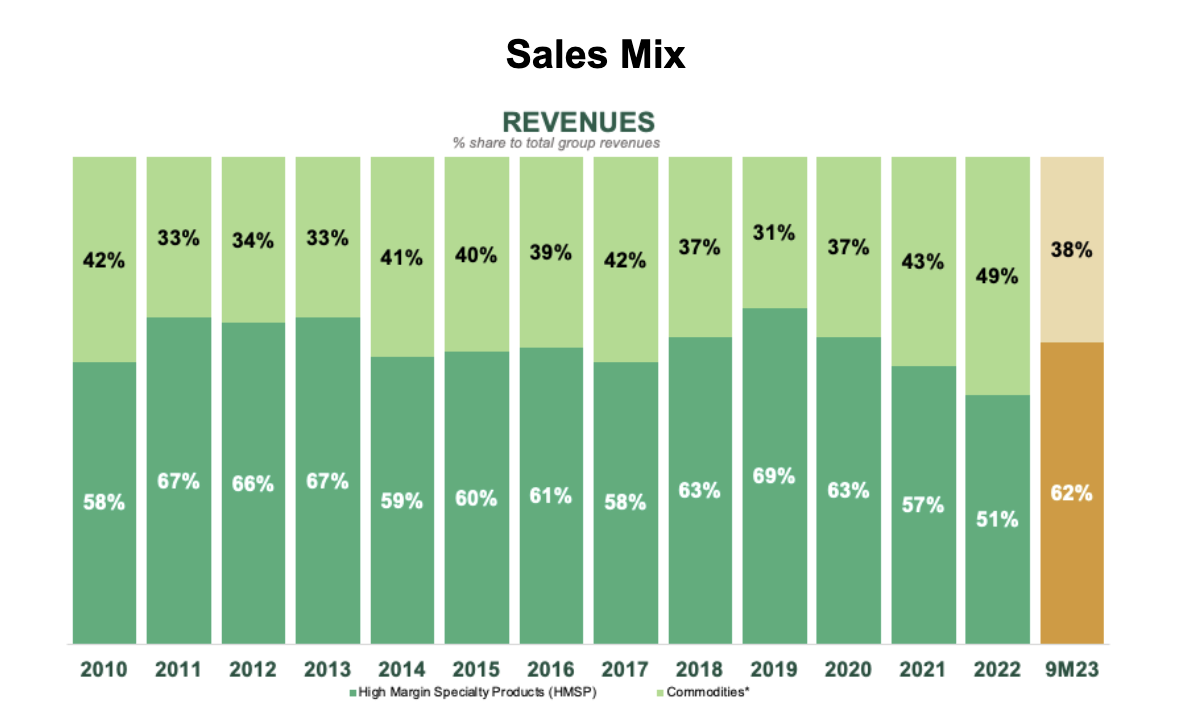

Sales mix back to pre-pandemic level; Margins recover sharply

While events over the past three years have resulted in a change in sales mix favoring commodities, 9M23 saw a reversal of this trend with High Margin Specialty Products (HSMP) revenue contribution back to pre-pandemic level at 62% from 51% in FY22. This, in turn, resulted in a 4.4 ppts improvement in blended gross profit margins to 17.4%.

Over time, as commodity sales continue to normalize and as the company continues to allocate much of its resources in growing the HMSP business, D&L expects to see a continued increase in HMSP revenue contribution.

Nonetheless, while commodity products have lower margins, the company intends to keep this segment as it continues to have a strategic importance in the overall business in the form of 1) maintaining customer goodwill, 2) protecting HMSP business by blocking off potential competitors, 3) covering some of the fixed costs, and 4) assuring the quality of HMSP raw materials.

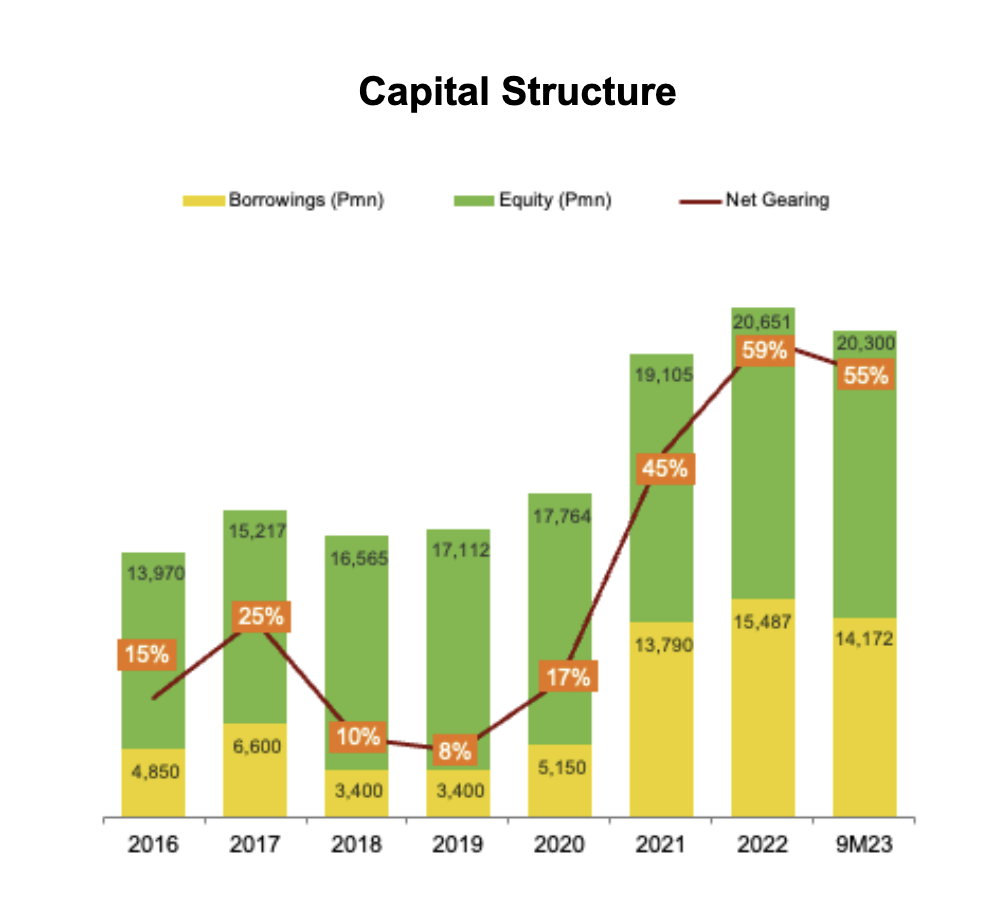

Free Cash Flows turned positive while debt level started coming down; Highest confidence in ability to service bonds maturing in 2024 and 2026

As the company moves past peak capex with the completion of its Batangas plant, coupled with the normalization of commodity prices, the company’s free cash flows (FCF) turned positive for the first time in two years. In 9M23, the company’s FCF stood at positive P2.5 billion vs negative P1.7 billion and negative P3.4 billion booked in FY22 and FY21, respectively.

Meanwhile, the company’s debt level has started to come down. In 9M23, total outstanding debt stood at P14.2 billion, lower than the P15.5 billion debt in FY22. As there are no other major capex planned aside from the expansion plan in Batangas, the improvement in the FCF gives the company the financial flexibility to further reduce its debt level over time.

As of end-September 2023, net gearing has likewise decreased from a peak of 61% in September 2022 to 55%, which remains to be a conservative level. Interest cover stood at 7x while the average interest rate increased to 5.65% from 4.7% in full year 2022. The P5 billion maiden bond offering of the company issued in September 2021 is helping cushion the recent increase in interest rates. The bonds carry a coupon rate of 2.8% p.a. and 3.6% p.a. for 3-year and 5-year tenors, respectively. These would have been significantly higher at approximately 6.7% for the 3-year tenor and 6.8% for the 5-year tenor if the company were to issue the bonds today.

With improving free cash flows, normalization of capex needs, as well as the continued optimism on the future prospects of the business, D&L has the highest confidence in its ability to service its bonds maturing in 2024 and 2026.

Segment results: Improvements seen in Food Ingredients, Specialty Plastics and Consumer Products ODM

Food Ingredients

The food ingredients group showed encouraging results for the period with 9M23 earnings managing to grow by 1% YoY despite the incremental costs related to the new plant in Batangas. On a gross profit level, which excludes the effect of the incremental expenses, the recovery was more apparent given the 27% increase YoY in 9M23.

The positive result was mainly driven by a combination of better margins and a pick up in HMSP volumes. With the normalization of commodity prices, the food ingredients business saw its margin recover sharply, increasing by 6.8 ppts in 9M23. Meanwhile, HMSP volumes picked up sharply in 3Q23, up +16% YoY. This brought HMSP volume growth to 2% in 9M23, reversing the 5% decline recorded in 1H23. With the peak season yet to come and as the economy continues to open up, further recovery is anticipated for the Food Ingredients business.

Consumer Products ODM

Consumer Products ODM segment saw its income grow by 34% YoY in 9M23. This resulted in the significant increase of the segment’s income contribution to the group which stood at 12% for the period from a mere 7% income contribution in full-year 2022. The strong growth was mainly driven by the continued reopening of the economy and the resumption of face-to-face activities which fuelled demand for many personal care products. Total volume for the segment was up 65% YoY.

Specialty Plastics

While the specialty plastics division was off to a slow start this year, with earnings falling as much as 20% YoY in the first half of the year, the third quarter posted a turnaround of results with earnings growing by 36% YoY. This brought 9M23 earnings decline to just 5% YoY.

The normalization of semiconductor supply globally has prompted a bounce back in the demand for engineered polymers used for automotive applications. As a result, volumes picked up sharply in 3Q23, up 27% YoY. This reversed the 4% volume decline recorded in 1H23, bringing 9M23 volume growth to 6% YoY.

Over the long term, this division is expected to continue to grow fuelled by the company’s R&D investments that are aimed at developing new applications for its products and introducing new technologies that will make plastics more economical and environmentally-friendly at the same time. The company is set to launch a new alternative to plastics that is equally durable and cost-competitive but is renewable, sustainable, and made from indigenous materials.

Chemrez

The stellar performance of Chemrez last year with its FY22 earnings growing by 47% YoY set up a high base for this year. However, a confluence of events such as 1) high inflation and weaker consumer spending, 2) early onset of the rainy season affecting the demand for construction materials, and 3) highly competitive landscape in the biodiesel business putting pressure on margins resulted in an earnings decline of 53% YoY in 9M23.

While this year is proving to be challenging, there are several catalysts on the horizon which should support medium to long-term growth. This includes 1) the potential hike in mandatory biodiesel blend, 2) additional capabilities with the commercial operations of the Batangas plant that will enable the company to do deeper innovations and manufacture higher value-added products, and 3) the company’s aggressive export thrust with the appointment of distributors in key export markets.

D&L champions high impact sustainability initiatives

D&L Industries has embraced a holistic approach to sustainable innovation, long before the term “ESG” became mainstream. With R&D at the company’s core, D&L is relentless in developing products that answer the needs of its customers while at the same time staying attuned to the needs of the planet. In the global scene, D&L is seen as an advocate for sustainable products derived from sustainable materials such as coconut oil, given its extensive technical knowhow and wide array of product offerings.

With its state-of-the-art manufacturing facility in Batangas, D&L is spearheading a paradigm shift in its approach towards sustainability. With the new capabilities that the Batangas plant will bring, D&L aims to offer turnkey solutions to customers that are both economically and environmentally friendly.

D&L envisions empowering brands globally to make a meaningful shift towards high impact sustainability initiatives in the manufacturing of their products by giving them the option to buy direct from source. The direct from source approach simply means converting raw materials into finished goods in the country of raw material origin, instead of going through multi-leg production stages which usually happen across different locations in the globe. This naturally translates into simpler logistics, less wastage, lower costs, higher efficiency, and as such, significantly cutting down the carbon footprint (C02) of the entire supply chain.

D&L is gearing up towards launching a full range of shelf-ready products for its export customers, made from coconut oil, for the personal and baby care, cosmetics and beauty care, household cleaning, health and nutrition, and food and vegetable oils categories that are sustainable, natural, and organic. This initiative offers a plug-and-play solution for global brand owners who are looking to beef up their sustainable product offerings. Under this strategy, D&L will primarily target export customers who do not have the proximity to the source and instead would traditionally go through multiple layers of production before their products get into its final form and ready for end-customer purchase or consumption.

-end-

D&L Industries is a Filipino company engaged in product customization and specialization for the food, chemicals, plastics and consumer products ODM industries. The company’s principal business activities include manufacturing of customized food ingredients, specialty raw materials for plastics, and oleochemicals for personal and home care use. Established in 1963, D&L has the largest market share in most of the industries it serves, as well as long-standing customer relationships with the Philippines’ leading consumer and manufacturing companies. It was listed on the Philippine Stock Exchange in December 2012. For more information, please visit https://www.dnl.com.ph/investors/.

This press release may contain some “forward-looking statements” which are subject to a number of risks and uncertainties that could affect D&L’s business and results of operations. Although D&L believes that expectations reflected in any forward-looking statements are reasonable, D&L does not guarantee future performance, action or events.

INVESTOR RELATIONS CONTACT

Crissa Marie U. Bondad

Investor Relations Manager – D&L Industries Inc.

+632 8635 0680

crissabondad@dnl.com.ph / ir@dnl.com.ph