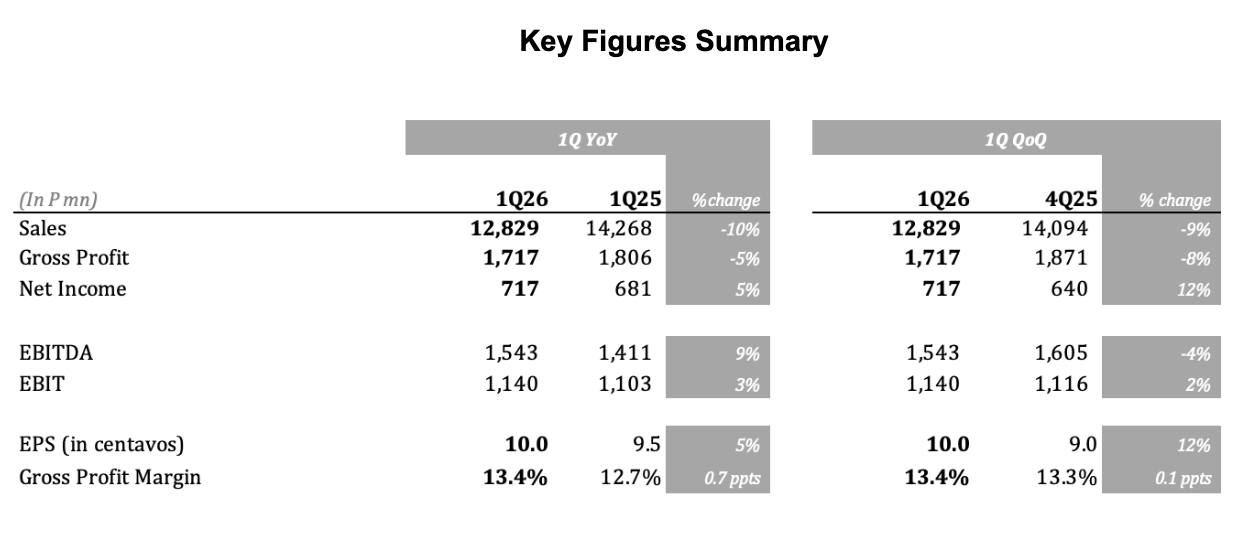

May 6, 2026 – D&L Industries’ recurring net income reached P717 million, or earnings per share of P0.10 in the first quarter of 2026 (1Q26). This is higher by 5% YoY and 12% QoQ, amidst the high uncertainty and volatility for the period due to the war in the Middle East. Earnings growth was mainly driven by the improvements in margins, as well as the consistent profitability at our Batangas plant, which booked its 6th consecutive profitable quarter.Management perspective and outlook

May 6, 2026 – D&L Industries’ recurring net income reached P717 million, or earnings per share of P0.10 in the first quarter of 2026 (1Q26). This is higher by 5% YoY and 12% QoQ, amidst the high uncertainty and volatility for the period due to the war in the Middle East. Earnings growth was mainly driven by the improvements in margins, as well as the consistent profitability at our Batangas plant, which booked its 6th consecutive profitable quarter.Management perspective and outlook

“Despite a continued challenging first quarter, we delivered 5% earnings growth, underscoring the resilience of our business model. Over the past periods, we have navigated significant volatility—from a sharp surge in coconut oil prices, one of our key raw materials, to the recent oil price shocks arising from geopolitical tensions in the Middle East. The essential nature of our products, catering to basic needs, provides a stable foundation even during periods of disruption. At the same time, our diversified business model offers resilience, allowing strength in one segment to offset softness in another,” remarked D&L President & CEO Alvin Lao.

“While the operating environment remains uncertain—marked by geopolitical tensions, elevated oil prices, inflationary pressures, and higher interest rates—we are confident in our ability to emerge stronger from each cycle. Periods of disruption also present opportunities. Ongoing supply chain challenges enable us to further solidify our position as a reliable supplier and trusted partner, supporting customers with customized solutions in an increasingly complex business landscape,” Lao continued.

“Amid global uncertainties and domestic headwinds that have weighed on Philippine market valuations and liquidity, we continue to see compelling value in fundamentally strong businesses with long-term staying power. This is reflected in the continued share acquisition by Jadel, the Lao family’s holding company, which has increased its stake in DNL by approximately 4.4% since the pandemic. In 2025 and year-to-date 2026 alone, Jadel acquired about 106 million and 4 million shares, respectively. At current levels, the stock offers an attractive dividend yield of approximately 5.9%, based on dividends declared last year,” Lao concluded.

Margins continue to improve, with 1Q26 blended GPM up 0.7 ppt YoY and HMSP GPM up 2.8 ppts YoY

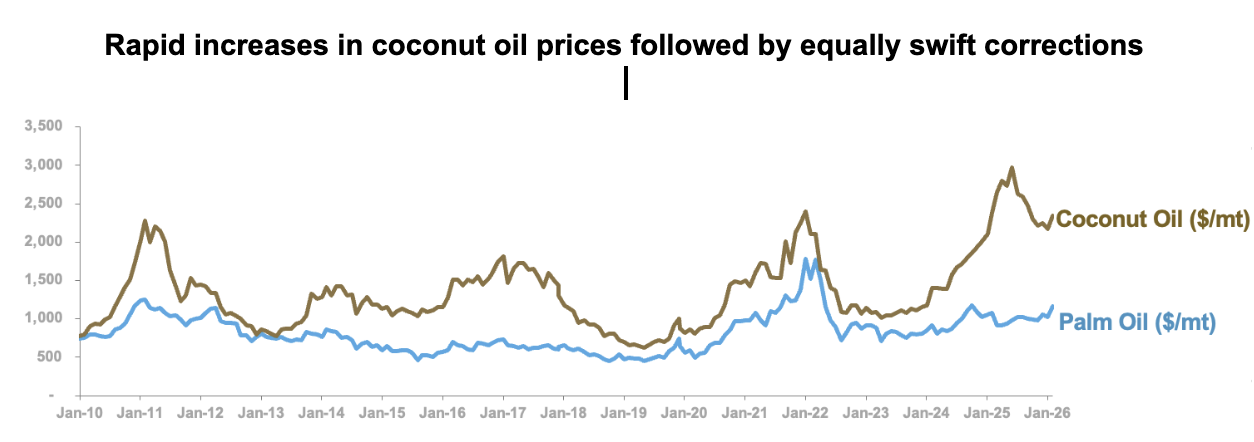

With coconut oil—one of our key raw materials—stabilizing at around USD 2,200/MT following a highly volatile period, margins continued to recover in 1Q26. Blended gross profit margin (GPM) improved to 13.4%, up 0.7 ppts YoY, reflecting easing input cost pressures and continued price pass-through. The High Margin Specialty Products (HMSP) segment delivered a more pronounced expansion, with GPM increasing by 2.8 ppts.

Meanwhile, the conflict in the Middle East pushed crude oil prices above USD 100/bbl and disrupted global supply chains, affecting several petrochemical-based raw materials. While near-term price movements remain uncertain, the company continues to rely on its price pass-through mechanisms and strong supplier partnerships to navigate the volatility. It also maintains approximately two months of inventory, providing a buffer against supply and price shocks.

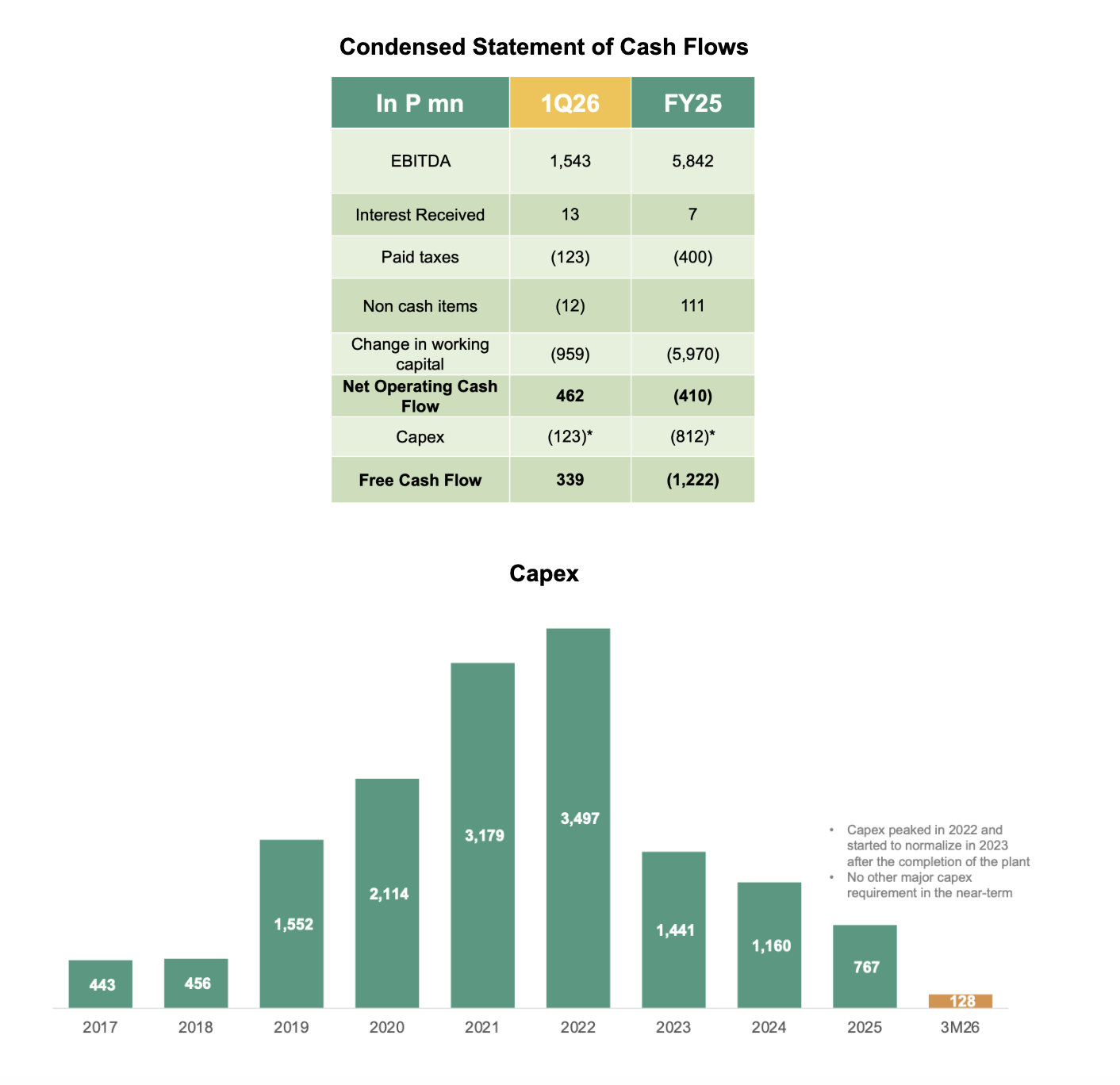

Free Cash Flows (FCF) turned positive for the quarter

FCF turned positive at P339 million for the period. This was largely a result of lower incremental working capital requirements with the normalization of coconut oil prices coupled with muted capex. Barring any price shocks and significant working capital requirements, the company expects FCF to remain positive. The company doesn’t anticipate any major capex spending in the near-term following the completion of the Batangas plant. With FCF turning positive and capex remaining muted, the company has ample room to delever its balance sheet.

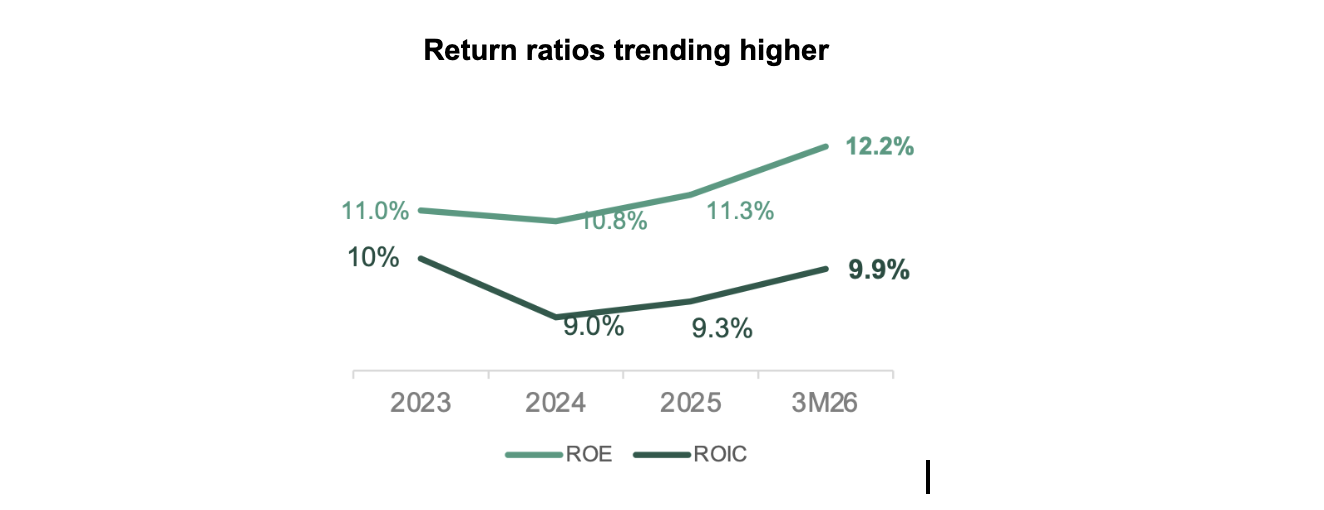

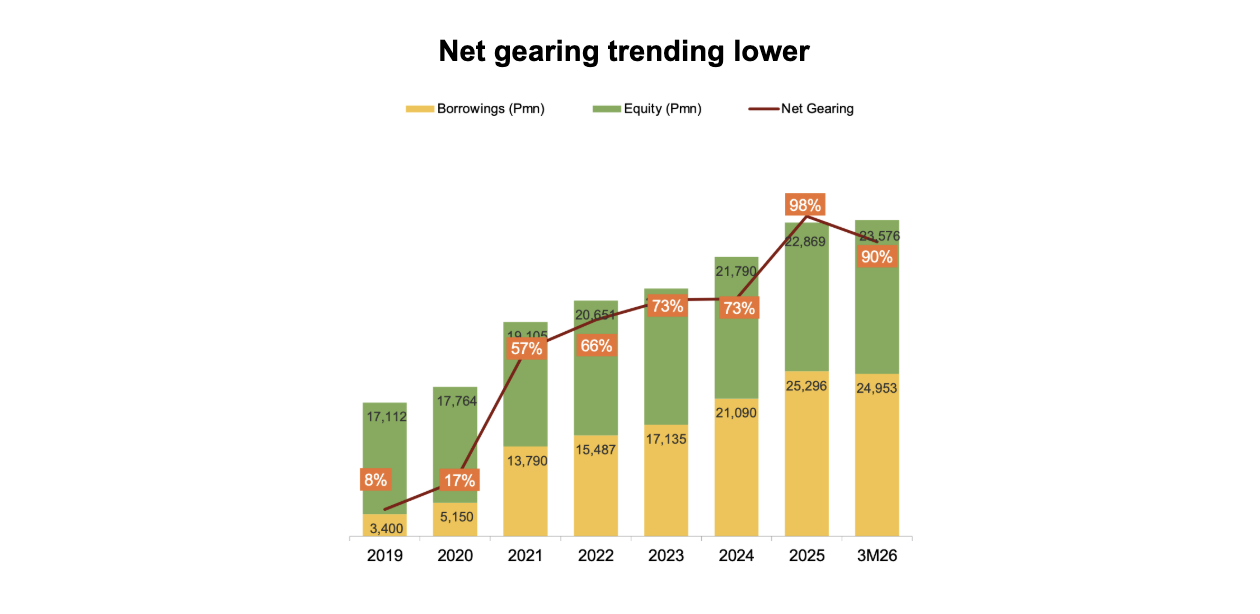

Return ratios continue to improve, while the balance sheet remains robust with gearing trending lower

Amid a challenging operating environment, the company delivered continued growth, driving further improvement in return ratios. ROE rose to 12.2% (+0.9 ppt vs end-2025), while ROIC increased to 9.9% (+0.6 ppt vs end-2025). As the Batangas plant ramps up and contributes more meaningfully to earnings, return ratios are expected to continue improving.

Meanwhile, the company’s balance sheet remained in a solid position even with the huge capex and unprecedented increase in commodity prices over the past couple of years. As of end-March 2026, interest cover remained at a comfortable level of 3x. Net gearing started to trend lower at 90% in 1Q26 from 98% as of end-December 2025. Average cost of debt was slightly lower at 5.9% vs 6.01% as of end-December 2025.

Segment Results

Food Ingredients

The Food Ingredients business saw a softer start to the year, with volumes declining 28% YoY and revenues down 16% YoY, resulting in a 69% YoY drop in earnings. This largely reflects ongoing portfolio optimization – the rationalization of lower-margin commodity exposure – as well as a high base in the prior period when volumes grew 33% YoY — a level not sustained this quarter amid external headwinds. As a net fuel importer, the Philippines was negatively affected by the oil price shock arising from geopolitical tensions, which raised food input costs and dampened foot traffic in certain segments of the food industry.

Encouragingly, margins showed early signs of recovery on a sequential basis, with blended GPM improving by 0.5 ppt QoQ. On a YoY basis, HMSP GPM expanded by 4.1 ppts, reflecting a stronger contribution from higher-value segments. As portfolio optimization progresses and coconut oil prices continue to normalize, the segment is well-positioned for more stable and improved profitability moving forward.

Chemrez

Chemrez sustained its strong growth momentum in 1Q26, with earnings rising 34% YoY, building on an exceptional 96% YoY growth in FY25. This performance was driven primarily by robust export sales of higher value-added coconut-derived products, as the company continues to expand into new markets and develop broader product applications.

Looking ahead, Chemrez remains optimistic about its medium-term outlook. With the Batangas plant now fully operational, Chemrez is well-positioned to serve a wider global customer base and scale up the production of higher value-added, sustainable ingredients.

Specialty Plastics

The Specialty Plastics segment delivered solid performance for the period, with earnings increasing 22% YoY, driven by 11% volume growth and a 0.4 ppt expansion in margins.

Amid supply chain disruptions due to the war in the Middle East affecting petroleum-derived products, a key raw material in the plastics industry, the company was able to cement its position as a reliable partner to its customers by demonstrating its ability to secure critical inputs and ensure continuity of supply in a challenging environment.

Over the longer term, successful new product developments—built on decades of R&D — continue to support margin expansion. The segment remains well-positioned for sustained growth, underpinned by ongoing investments in innovation and a focus on delivering higher-value, sustainable plastic solutions aligned with evolving customer requirements.

Consumer Products ODM

Consumer Products ODM delivered strong growth, with earnings rising 65% YoY, driven by 14% volume growth and a 2.2 ppt expansion in margins as the Batangas plant continues to ramp up. The segment is well-positioned for further growth, supported by additional capacity from the new facility and ongoing efforts to expand its presence in export markets.

-end-

D&L Industries is a Filipino company engaged in product customization and specialization for the food, chemicals, plastics and consumer products ODM industries. The company’s principal business activities include manufacturing of customized food ingredients, specialty raw materials for plastics, and oleochemicals for personal and home care use. Established in 1963, D&L has the largest market share in most of the industries it serves, as well as long-standing customer relationships with the Philippines’ leading consumer and manufacturing companies. It was listed on the Philippine Stock Exchange in December 2012. For more information, please visit https://www.dnl.com.ph/investors/.

This press release may contain some “forward-looking statements” which are subject to a number of risks and uncertainties that could affect D&L’s business and results of operations. Although D&L believes that expectations reflected in any forward-looking statements are reasonable, D&L does not guarantee future performance, action or events.

INVESTOR RELATIONS CONTACT

Crissa Marie U. Bondad

Investor Relations Manager – D&L Industries Inc.

+632 8635 0680

crissabondad@dnl.com.ph / ir@dnl.com.ph