March 29, 2023 – For the FY2022, D&L Industries recorded its highest ever net income, demonstrating a full recovery from the COVID pandemic amidst a confluence of macroeconomic headwinds. The P3.3 billion of earnings exceeds the company’s previous record of net income achieved in 2018. The company’s full year 2022 net income stood at P3.3bn, higher by 26% YoY. In 4Q22 alone, earnings were up 62% YoY to P777 million. These results outperformed expectations and were mainly driven by strong consumer spending amidst wider economic reopening and the company’s exports undergoing resilient growth. The three biggest business segments of the company – food ingredients, oleochemicals and other specialty chemicals, and specialty plastics – all booked positive earnings growth for the year which were either at record highs or slightly below.

D&L’s robust earnings for the year demonstrate its ability to weather various macroeconomic conditions given its diversified businesses, the essential nature of the products it manufactures, and its ability to adjust its selling prices regularly.

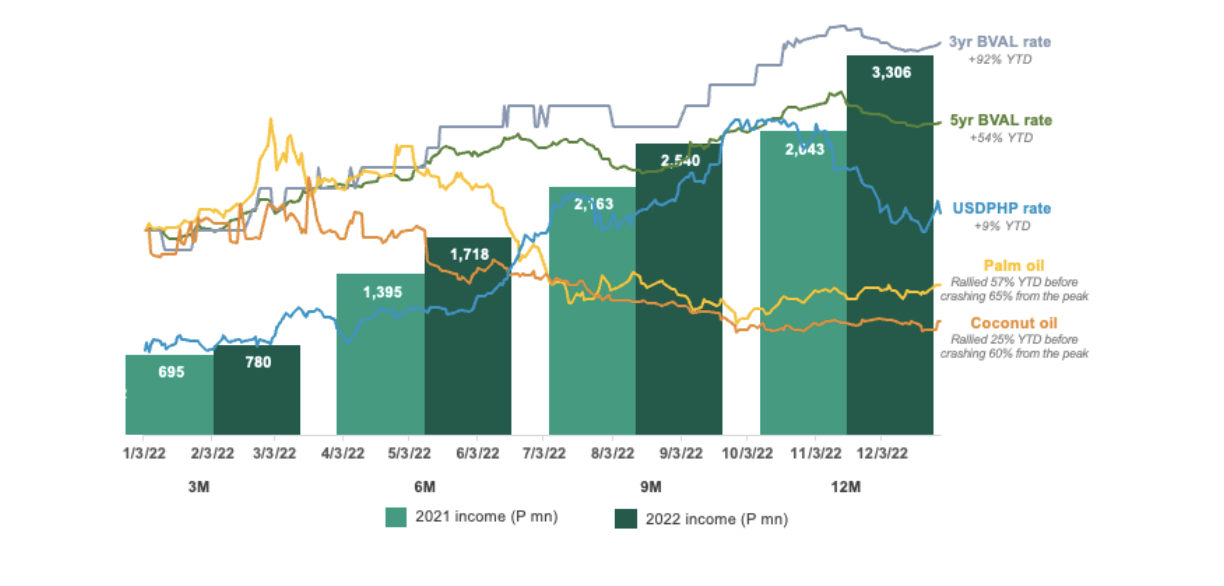

Volatile commodity prices, higher interest rates, and weak peso had minimal impact on earnings

Management Perspective

“Just when we thought that we were at the tail end of the challenges brought about by the pandemic, 2022 presented a fresh set of challenges which were mostly on the macroeconomic front. Nonetheless, our record earnings this year demonstrated the resilience that we have built over the years through the various crises that we have gone through,” remarked President & CEO Alvin Lao.

“While risk remains in the form of elevated inflation, threat of a US recession, and a global banking turmoil, we are optimistic and focused on our long-term structural growth story. We look forward to the commercial operations of our Batangas plant by mid this year. This plant will be transformational for us from a sustainable growth perspective. It will add the capabilities that will allow us to increase our relevance in the overall production chain and service new and bigger customers globally,” Lao concluded.

Record income despite a confluence of macroeconomic headwinds

D&L Industries achieved record income for the period despite a confluence of volatile raw material prices, higher inflation and interest rates, a weak peso, and an Omicron surge early in the year. The better-than-expected earnings were mainly driven by the continued reopening of the Philippine economy and stronger company exports. With the lowest alert level in place and the lifting of the mask mandate, economic activity and consumer mobility continue to pick up as people become more comfortable going out. This is evidenced by the higher consumer traffic in retail establishments, higher occupancy in restaurants, and higher frequency of both domestic and international flights. Meanwhile, D&L’s export business is proving to be resilient with Chemrez’s earnings growing by 47% in FY22. The growth was largely driven by the higher export market penetration and higher demand for sustainable, organic, and natural coconut oil-based raw materials used in various health, personal, and home care products.

Overall, D&L’s full year 2022 net income stood at P3.3bn, higher by 26% YoY. In 4Q22 alone, earnings were up 62% YoY to P777 million. This was largely driven by the meaningful margin recovery in 4Q22 compared to the same period last year. On a quarter-on-quarter basis, however, earnings were lower by 5%. This was mainly attributable to the high volume of orders from earlier periods, with some customers still consuming their excess inventory in 4Q22. The company expects this to normalize in the coming months.

HMSP and commodity margins are back to pre-pandemic levels

Prices of some of the company’s key raw materials such as coconut and palm oil have been volatile for the year, driven by global events such as the Russia-Ukraine conflict and the temporary ban on export of palm oil by Indonesia. Average coconut oil and palm oil prices have rallied 25% YTD and 57% YTD, respectively, before correcting by 60% and 65%, respectively, from recent peaks.

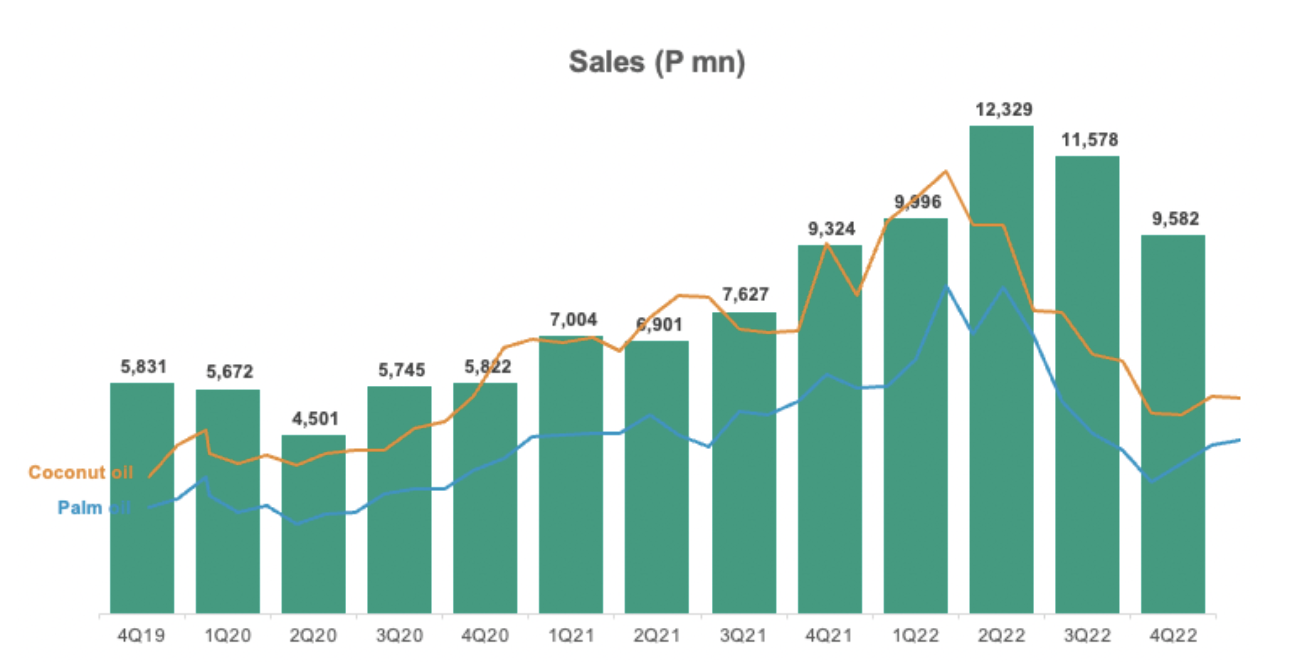

D&L maintains its ability to weather the volatility in raw material prices, as the company adjusts its selling prices regularly to reflect higher input costs. As shown in the chart below, D&L’s revenues have generally moved in tandem with the movements in the commodity prices, evidencing the company’s ability to pass on raw material prices.

While 2022 was characterized by sharp increases in commodity prices at the beginning of the year which resulted in margin contraction as there is generally a 30-45 day time lag before the company can start adjusting selling prices, margins have started to recover in the second half of the year as commodity prices have started to stabilize. In 4Q22 alone, HMSP (High Margin Specialty Products) and commodity margins rebounded sharply, up 6.4ppts and 4.5ppts YoY, respectively, and are already back to pre-pandemic levels.

Beyond the margin recovery from the normalization of commodity prices, the company sees ample room for margins to go up further over the long term. With the unprecedented business and supply chain disruptions over the past two years, D&L has cemented its position as a reliable partner and supplier to its customers. This should pave the way for better business opportunities as the macroeconomic environment improves. Given the company’s extensive R&D and manufacturing capabilities, there are also plenty of opportunities to develop higher value added products as consumer tastes and preferences evolve.

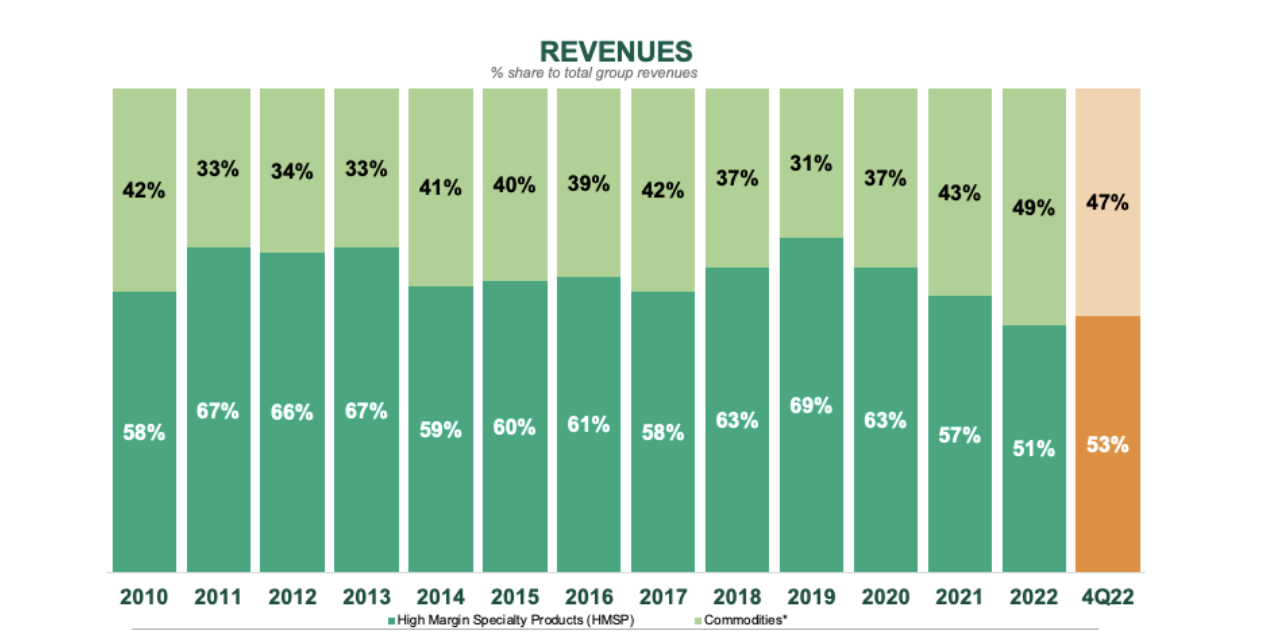

Sales mix tilting back to HMSP

The events which transpired over the past two years have resulted in a change in sales mix favoring commodities. For instance, the pandemic resulted in a demand shift towards more basic raw materials while the various supply chain disruptions resulted in market share gains in the commodity segment as smaller commodity players were not able to operate. As a result of this, the company’s commodity business saw extraordinary growth in the period, translating to a 50/50 HSMP to commodity sales mix as of the first nine months of 2022 vs a 69/31 HMSP-commodity sales mix pre-pandemic.

In 4Q22, however, the company’s sales mix has started tilting back to HMSP as its revenue contribution inched up to 53%, bringing FY22 revenue contribution to 51%. Over time, as commodity sales normalize and as the company continues to allocate much of its resources in growing the HMSP business, D&L expects to see a continued increase in HMSP revenue contribution.

While commodity products have lower margins, the company intends to keep this segment as it continues to have a strategic importance in the overall business in the form of 1) maintaining customer goodwill, 2) protecting HMSP business by blocking off potential competitors, 3) covering some of the fixed costs, and 4) assuring the quality of HMSP raw materials.

Export is a bright spot

The exports division continued its positive momentum in FY22, with revenues jumping 33% YoY for the period. Export contribution to total revenues in FY22 stood at 31%, evidencing the company’s commitment to diversify its revenue base by strategically growing its international customer base.

Coconut-based products under food and oleochemicals were the main drivers behind robust export growth in the period. Coconut oil continues to gain traction in the global market due to its perceived natural antiviral, antibacterial, and antifungal properties. In addition, coconut oil remains a valued, sustainable substitute for petroleum-based raw materials used in many applications such as personal hygiene and home cleaning products. Going forward, the company expects its foothold in coconut oil-based exports to strengthen especially as the company builds its capabilities to serve a wider array of international customers.

Batangas expansion will position the company for long-term growth and enable the achievement of strategic priorities

D&L remains committed to its Batangas expansion which is set to start commercial operations in 2023. Total estimated capex for the new plant is around P10.2 billion. As of end-December 2022, the company has spent around P9.4 billion for the project. Once the Batangas plant is completed, capex is expected to decrease as there are no other major expansions currently planned, and free cash flows of the company may turn positive by this year.

In September 2021, the company executed its maiden bond offering, successfully raising P5 billion to help fund the capex for this expansion. These fixed rate bonds received the highest rating of Aaa by Philippine Rating Services Corporation (Philratings) and was 5x oversubscribed, allowing D&L to price its bond at among the lowest rates in Philippine corporate bond history. The issuance was also awarded by the Asset Magazine as the Best New Bond in the Philippines for the year 2021. For the bond rating renewal in 2022, Philratings has maintained its Aaa rating with a stable outlook demonstrating the company’s solid financial position and prospects.

D&L’s Batangas expansion will be instrumental to its future growth, as this facility will enable the company to develop more high value-added coconut-based products and penetrate new international markets. In the new normal, the company has successfully made significant in-roads in supplying various raw materials and even finished products in several relevant fast-moving consumer goods (FMCG) categories. It plans to further expand its global footprint and in the long-term, targets export sales to account for at least 50% of total revenue.

The facility will mainly cater to D&L’s growing export businesses in the food and oleochemicals segments. It will add the capability to manufacture downstream packaging, thus allowing the company to capture a bigger part of the production chain. For instance, while the company primarily sells raw materials to customers in bulk, the new plants will allow it to “pack at source”. This means that D&L will have the ability to process the raw materials and package them closer to finished consumer-facing products. This will enable D&L to move a step closer to its customers by providing customized solutions and simplifying their supply chain, which is of high importance given ongoing logistical challenges.

Operational and financial resilience

As the world gradually recovers from the pandemic, D&L is emerging more resilient than ever, having instituted various adjustments and operational contingencies. While there are renewed risks to global growth and recovery, the company believes that it is now in a far better position to thrive in an adverse environment and a potentially protracted economic recovery period. Moreover, as most products that the company manufactures cater to essential industries such as food, oleochemicals, plastics and other basic materials, the company sees continued strong demand ahead.

From a capital structure perspective, the company is in a solid position to withstand external pressures. As of end-December 2022, net gearing continues to remain manageable at 59%, interest cover at 18x, and average interest rate at 4.7%. The issuance of the P5 billion maiden bond offering of the company is helping cushion the recent increase in interest rates. The bonds carry a coupon rate of 2.7885% p.a. and 3.5962% p.a. for 3-year and 5-year tenors, respectively, which would have been significantly higher at approximately 6.4029% for the 3-year tenor and 6.6087% for the 5-year tenor if the company were to issue the bonds today.

Meanwhile, the cash conversion cycle for the period was lower at 99 days vs. 120 days in 2021, given lower inventory and account receivables days.

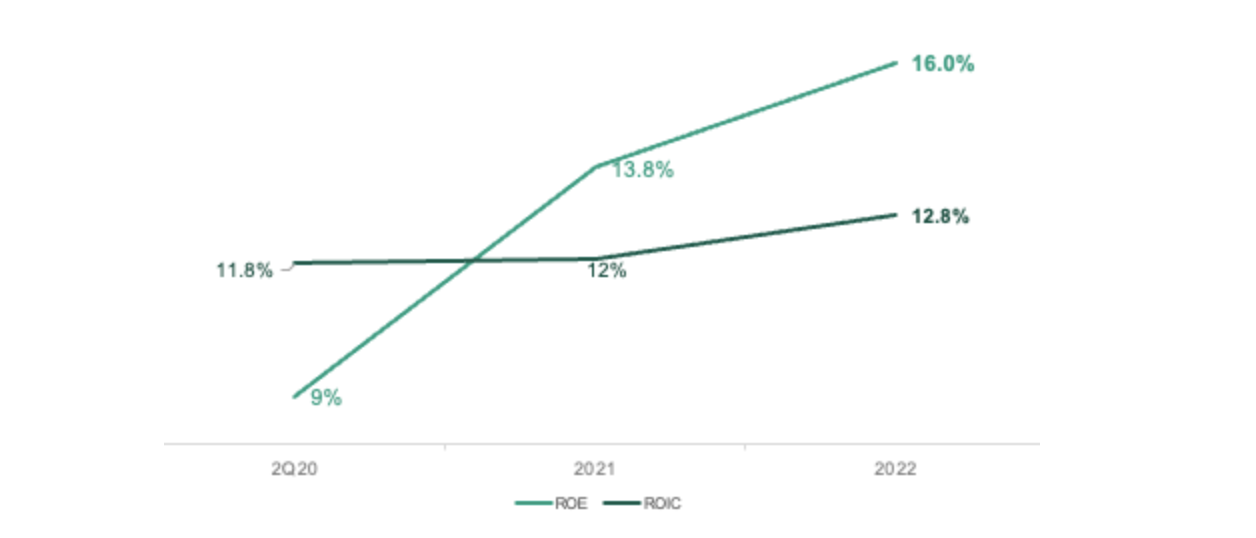

Overall, the company’s profitability ratios remain healthy. Return on Equity (ROE) and Return on Invested Capital (ROIC) stood at 16% and 13%, respectively, in FY22.

ROE & ROIC up significantly from the low in 2Q20

D&L champions high impact sustainability initiatives

D&L Industries has embraced a holistic approach to sustainable innovation, long before the term “ESG” became mainstream. With R&D at the company’s core, D&L is relentless in developing products that answer the needs of its customers while at the same time staying attuned to the needs of the planet. In the global scene, D&L is seen as an advocate for sustainable products derived from sustainable materials such as coconut oil, given its extensive technical knowhow and wide array of product offerings.

With its upcoming state-of-the-art manufacturing facility in Batangas, D&L is spearheading a paradigm shift in its approach towards sustainability. With the new capabilities that the Batangas plant will bring, D&L aims to offer turnkey solutions to customers that are both economically and environmentally friendly.

D&L envisions empowering brands globally to make a meaningful shift towards high impact sustainability initiatives in the manufacturing of their products by giving them the option to buy direct from source. The direct from source approach simply means converting raw materials into finished goods in the country of raw material origin, instead of going through multi-leg production stages which usually happen across different locations in the globe. This naturally translates into simpler logistics, less wastage, lower costs, higher efficiency, and as such, significantly cutting down the carbon footprint (C02) of the entire supply chain.

D&L is gearing up towards launching a full range of shelf-ready products for its export customers, made from coconut oil, for the personal and baby care, cosmetics and beauty care, household cleaning, health and nutrition, and food and vegetable oils categories that are sustainable, natural, and organic. This initiative offers a plug-and-play solution for global brand owners who are looking to beef up their sustainable product offerings. Under this strategy, D&L will primarily target export customers who do not have the proximity to the source and instead would traditionally go through multiple layers of production before their products get into its final form and ready for end-customer purchase or consumption.

Segment Results

Food Ingredients

With the reopening of the economy, the food ingredients segment continues to recover as overall volume for the year was up 14% YoY. In addition, as commodity prices continue to stabilize, margins have likewise started to improve. In 4Q22 alone, the gross profit margin (GPM) for the segment was up 3.3ppts YoY resulting in a 82% jump in profits for the quarter. Overall, the food ingredients division managed to end the year with a net income growth of 10% YoY, reversing the 6% income decline recorded in 9M22.

This business was the segment most heavily affected by the pandemic, hence it is also expected to post the sharpest recovery post-pandemic. With quarantine restrictions now easing across the country and in the economic hub of Metro Manila, the company anticipates that further recovery is set to continue as fully vaccinated individuals are granted more freedom of movement, especially when frequenting restaurants, hotels, and the service industry.

Chemrez

With higher export market penetration and the strong demand for organic, sustainable, and natural coconut oil-based products, Chemrez booked a record income for the year which was up 47% YoY. Oleochemicals division, which was the main growth driver, saw its volume grow by 46% YoY and GPM increase by 3.7ppts.

Under the Oleochemicals division, the company sells various coconut oil derivatives which are categorized as either commodity (biodiesel) or high margin coconut oil-based products mostly for exports. As the economy continues to reopen, demand for biodiesel has started to pick up. Meanwhile, the high margin coconut-based products which are sustainable substitutes for petroleum-based raw materials used in many applications such as personal hygiene and home cleaning products continue to benefit from the increasing consumer awareness and preference for natural, organic, and sustainable products.

Plastics

Specialty plastics managed to end the year with an earnings growth of 11% YoY as the 1.2-ppt margin expansion more than offset the impact of the 14% YoY volume decline for the period. The disruptions brought about by the Omicron surge in January and the global shortage of semiconductor chips used in automotives resulted in lower demand for wire harnesses. Nonetheless, over the long term, the company expects this division to continue to grow fuelled by the company’s R&D investments that are aimed at developing new applications for its products and introducing new technologies that will make plastics more economical and environmentally-friendly at the same time.

Consumer Products ODM

With the continued economic reopening, the personal care division of the Consumer Products ODM segment saw its volume grow by 44% YoY in FY22. This offset the normalizing demand for disinfection and sanitation products as the world moves towards the tail end of the pandemic. In 4Q22 alone, earnings jumped 75% YoY, bringing the full year earnings decline to just 7% YoY from a decline of 23% YoY as of 9M22.

Despite the slight YoY earnings contraction, FY22 earnings were still well-above pre-pandemic income level recorded in FY19. D&L expects this segment to return to profit growth as quarantine restrictions continue to ease, leading to greater foot traffic in retail outlets and more consumers resuming the regular use of personal hygiene products.

-end-

D&L Industries is a Filipino company engaged in product customization and specialization for the food, chemicals, plastics and consumer products ODM industries. The company’s principal business activities include manufacturing of customized food ingredients, specialty raw materials for plastics, and oleochemicals for personal and home care use. Established in 1963, D&L has the largest market share in most of the industries it serves, as well as long-standing customer relationships with the Philippines’ leading consumer and manufacturing companies. It was listed on the Philippine Stock Exchange in December 2012. For more information, please visit https://www.dnl.com.ph/investors/.

This press release may contain some “forward-looking statements” which are subject to a number of risks and uncertainties that could affect D&L’s business and results of operations. Although D&L believes that expectations reflected in any forward-looking statements are reasonable, D&L does not guarantee future performance, action or events.

INVESTOR RELATIONS CONTACT

Crissa Marie U. Bondad

Investor Relations Manager – D&L Industries Inc.

+632 8635 0680

crissabondad@dnl.com.ph / ir@dnl.com.ph